Sagging College Pricing Power, pre-COVID

Sagging College Pricing Power, pre-COVID

Part 1 of a series starts with the Rocky Mountain state schools

Before COVID threw higher ed's finances into disarray, colleges saw eroding pricing power despite the strong economy Americans enjoyed in 2015-2019. While we could expect to see this erosion in certain private colleges, the weakness also showed up across the country, in many unexpected places. The erosion was so widespread that we will be making a point of identifying colleges which did not show it in their results.

For this study, we will rely on instituitional aid figures from IPEDS. This is not ideal in terms of mathematics - aid or discounting is a fiddly way of getting to market price - but it does illustrate how colleges experienced institutional dissonance as the cost of attendance determined by their formal tuition-setting mechanism was increasingly at odds with the real market.

We will start in a truly unexpected place: Rocky Mountain state schools. Before we dug into the numbers, we were expecting price pressure at some private colleges, in the area around Cleveland and Buffalo, and other eastern states close to the Canada border. The fact that the Rocky Mountain state schools were unable to raise their prices came as a surprise. These schools worked amid favorable demographic trends and, even within a flourishing US economy, the region outperformed. In fact, Colorado, Idaho and Utah had the fastest three personal income growth results in the country in 2019, per US Census numbers. These states were close to booming. And yet their colleges had to cut prices or face the consequences.

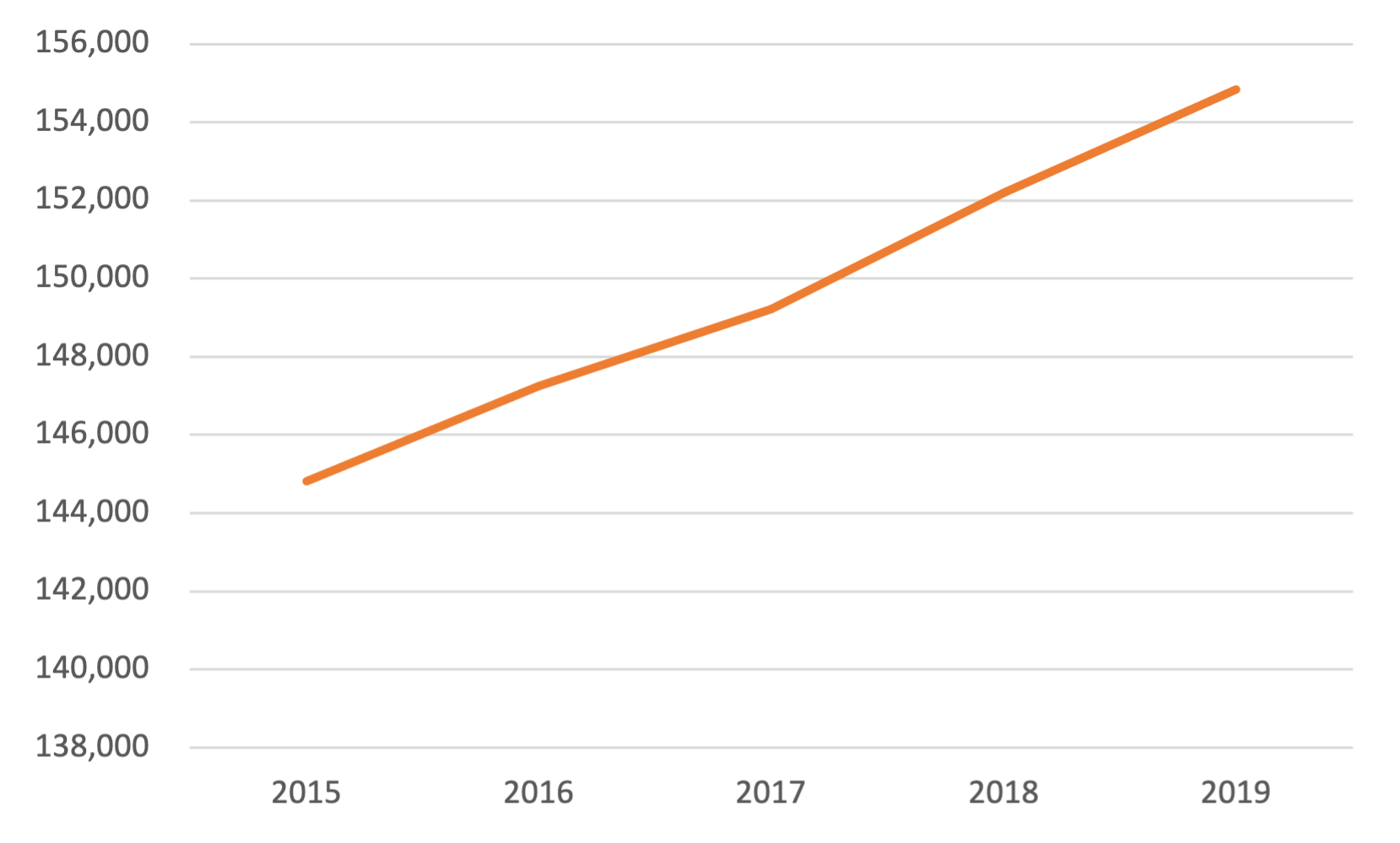

Favorable demographics

This price discounting took place in a favorable enrollment environment, with the Rocky Mountain region benefitting from a demographic tailwind amid steady growth in high school graduating classes.

Graduating classes in Colorado, New Mexico, Utah, Wyoming, Montana and Idaho. The chart uses older WICHE projections so as to include private high schools.

Soaring financial aid budgets

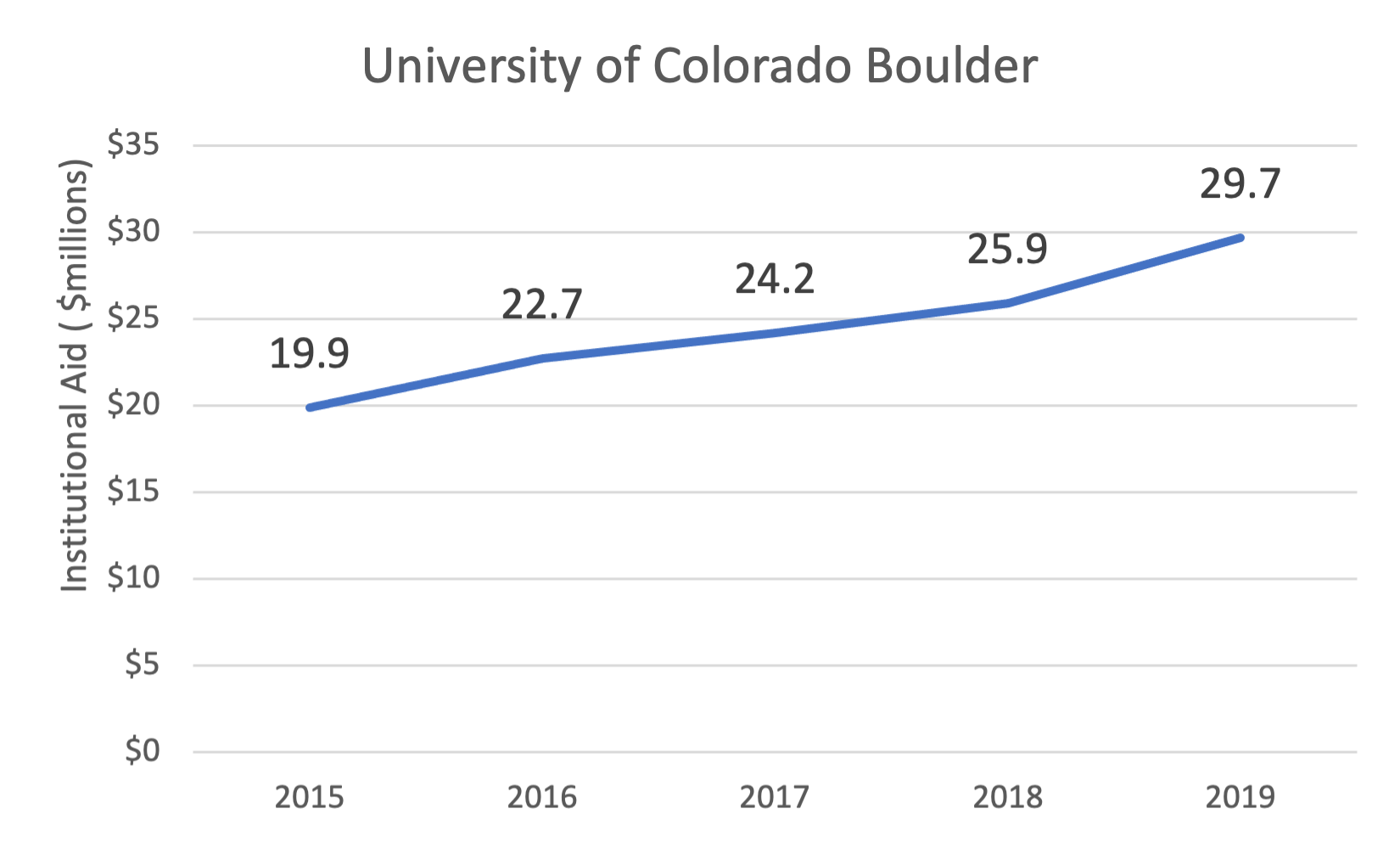

Most of the state schools which offered institutional aid were forced to increase their financial aid budgets to attract students. Let’s start with the one with the highest profile, Colorado’s Boulder campus:

All financial aid figures used in this series include both need and merit aid. IPEDS data.

Was Boulder's increased need to pony up financial aid due to competing for out-of-state students (Boulder's 2019 entering class was 45% out-of-state)? CTAS internal estimates indicate that a bit over half of this institutional aid was given to out-of-state students. But Colorado State in Fort Collins, with a lower number of out-of-state in that class (29%) and a lower proportion of aid granted to out-of-state students, shows an even steeper increase in financial aid outlays, though from a lower base.

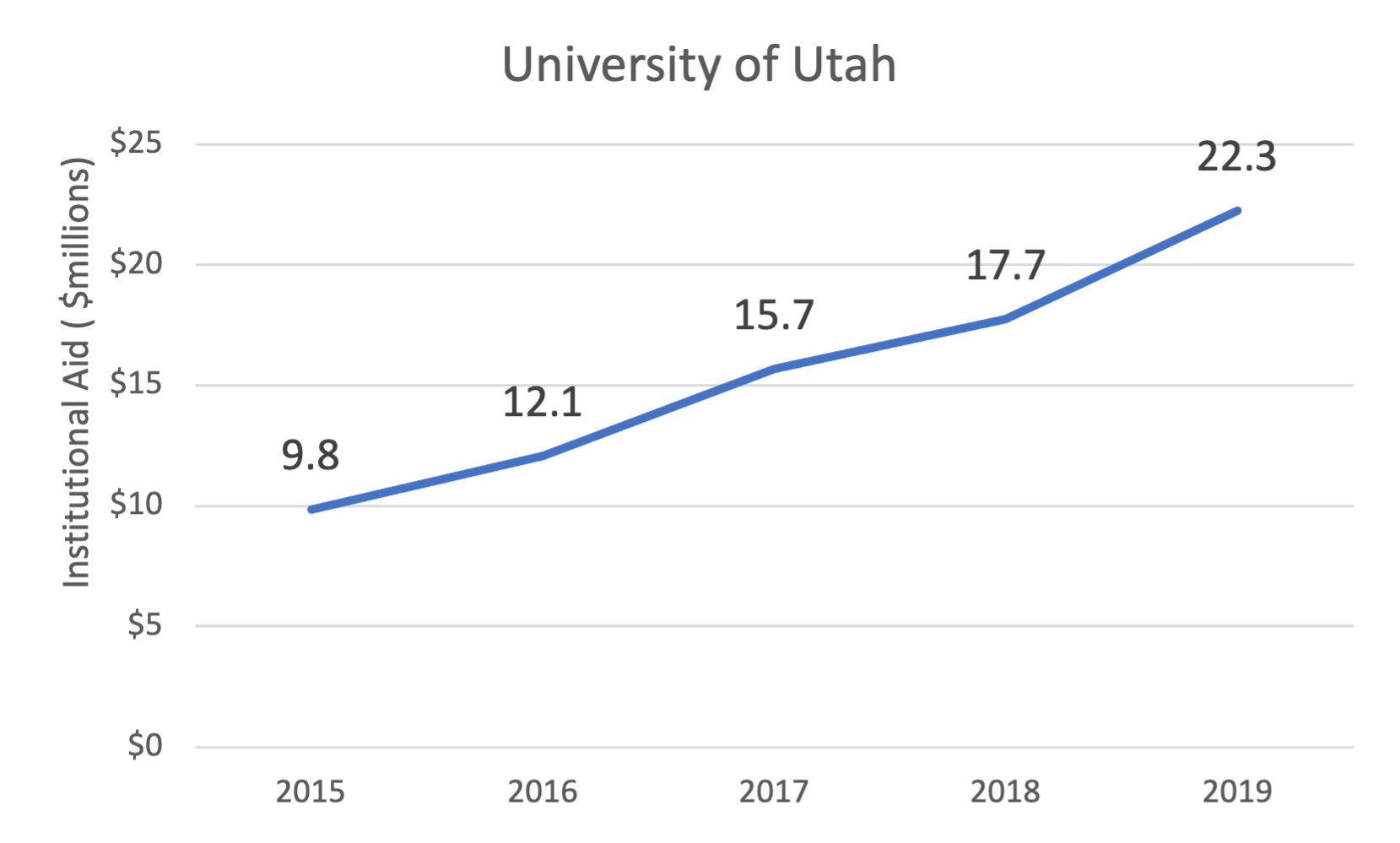

Take another example: the University of Utah in Salt Lake City. Like Colorado State, Utah enrolls 29% out-of-state students, making it primarily reliant on in-state recruitment. It was forced to more-than-double its financial aid outlays in just 4 years, from $10 million to $22.

The University of Utah was unusual in that it has become a more selective school: it admitted 81% of applicants in 2015 but just 62% in 2019. But its yield numbers have shown slight erosion despite the price discounting and increased selectivity.

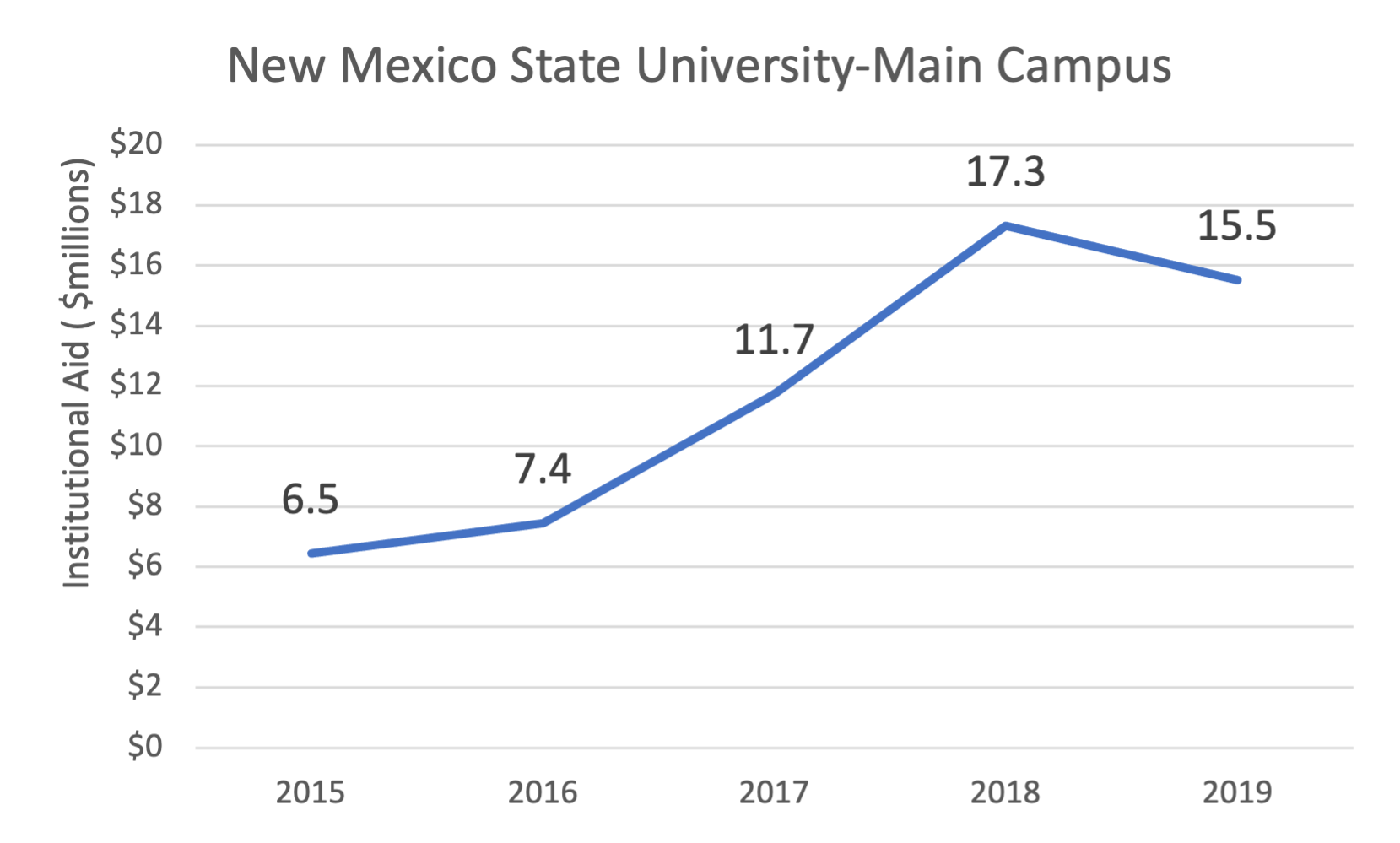

The steepest increase in financial aid of any of the schools took place at New Mexico State in Las Cruces, which took in 30% out-of-state students in its 2019 class, similar to the two schools above. NM State raised its institutional aid by 140% from 2015 through 2018, and on a per student basis easily more than doubling.

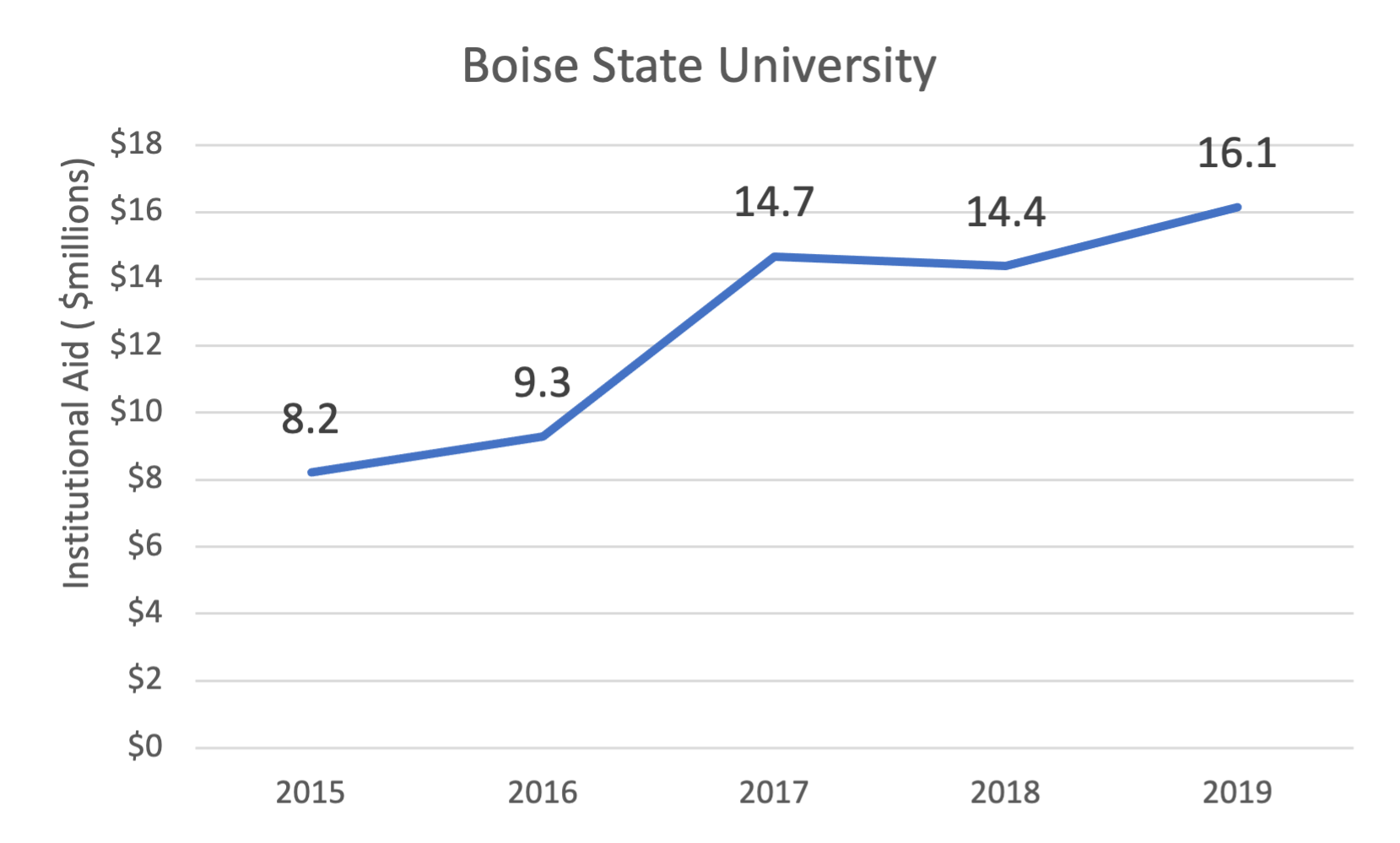

The University of Wyoming, Boise State and University of Idaho all showed the same pattern. Each had to roughly double their financial aid in the span of four years. Boise State is representative:

The two Idaho schools also saw sagging yields despite the amped up financial aid awards.

A couple of schools said “no” to higher financial aid

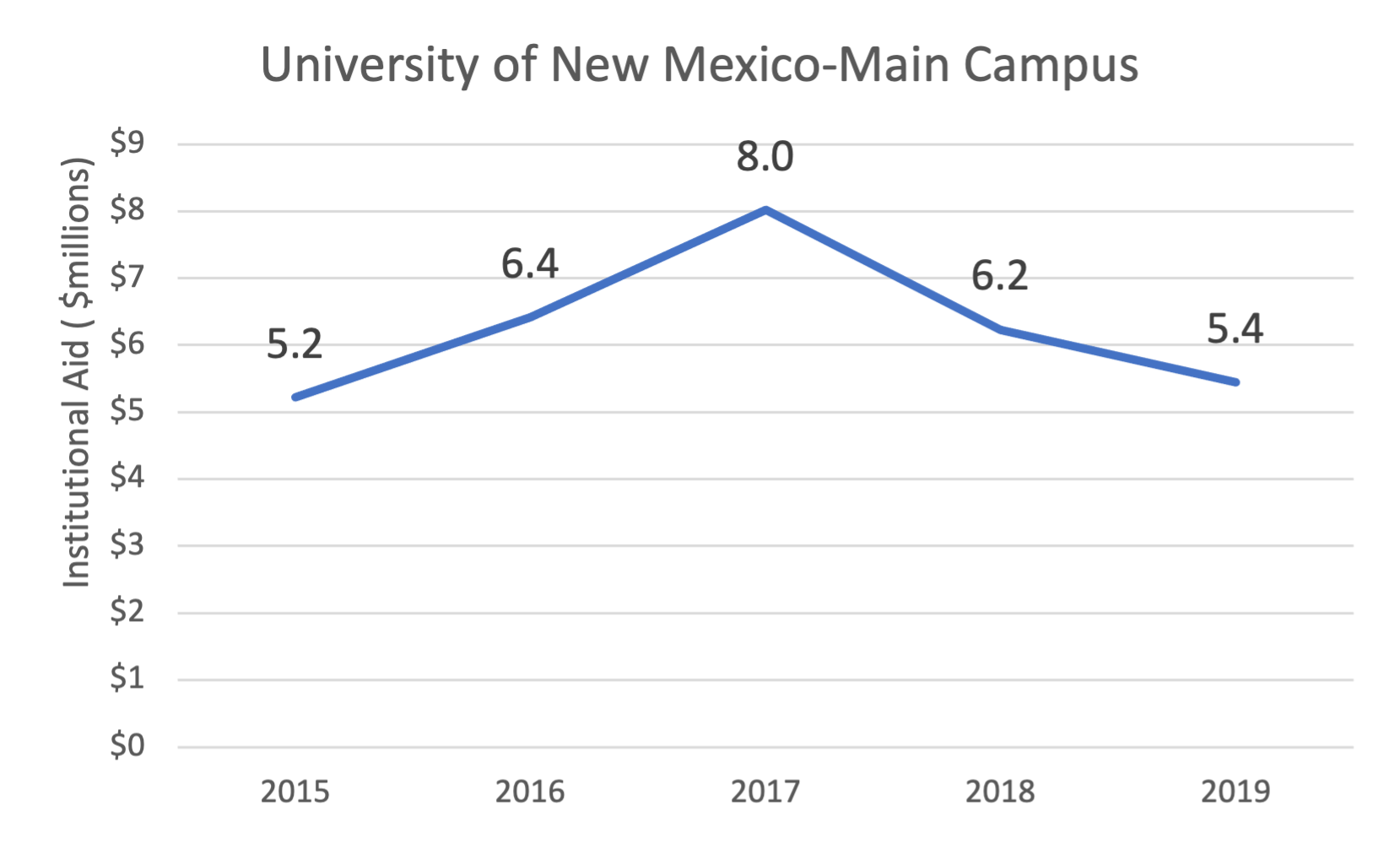

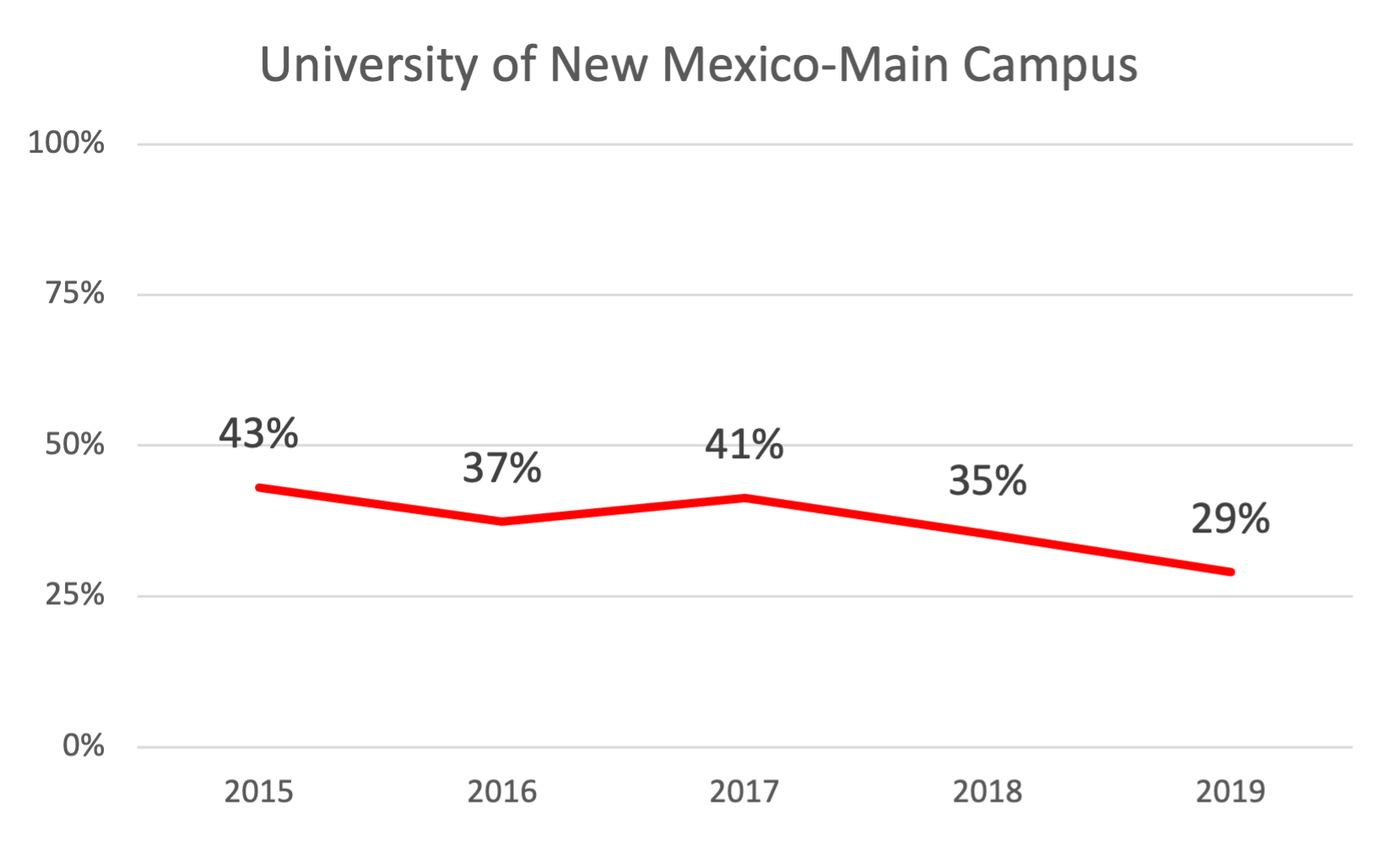

Equally significant is what happened to schools that held the line on discounts and financial aid. The flagship University of New Mexico in Albuquerque (UNM) said no to discounts, with 2019 total outlays approximately equal to 2015.

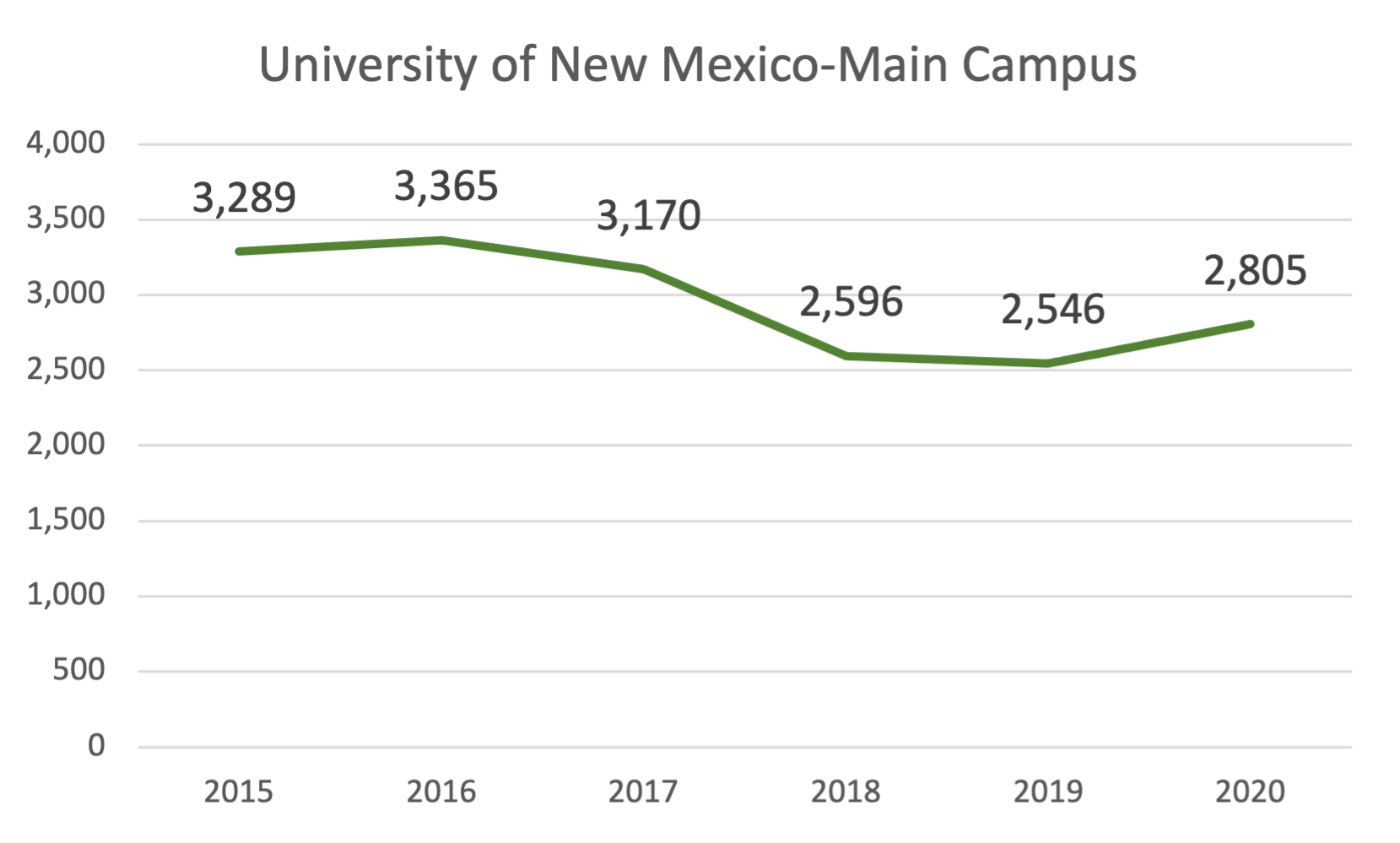

What happened? UNM saw its entering class of full-time students fall from 3,298 to 2,546 in 2019. Enrollment numbers were better in other years and the 2020 class did show an improvement, numbering about 2,800. But note that the cut in financial aid occurring in 2018 was matched with a clear decrease in enrollment.

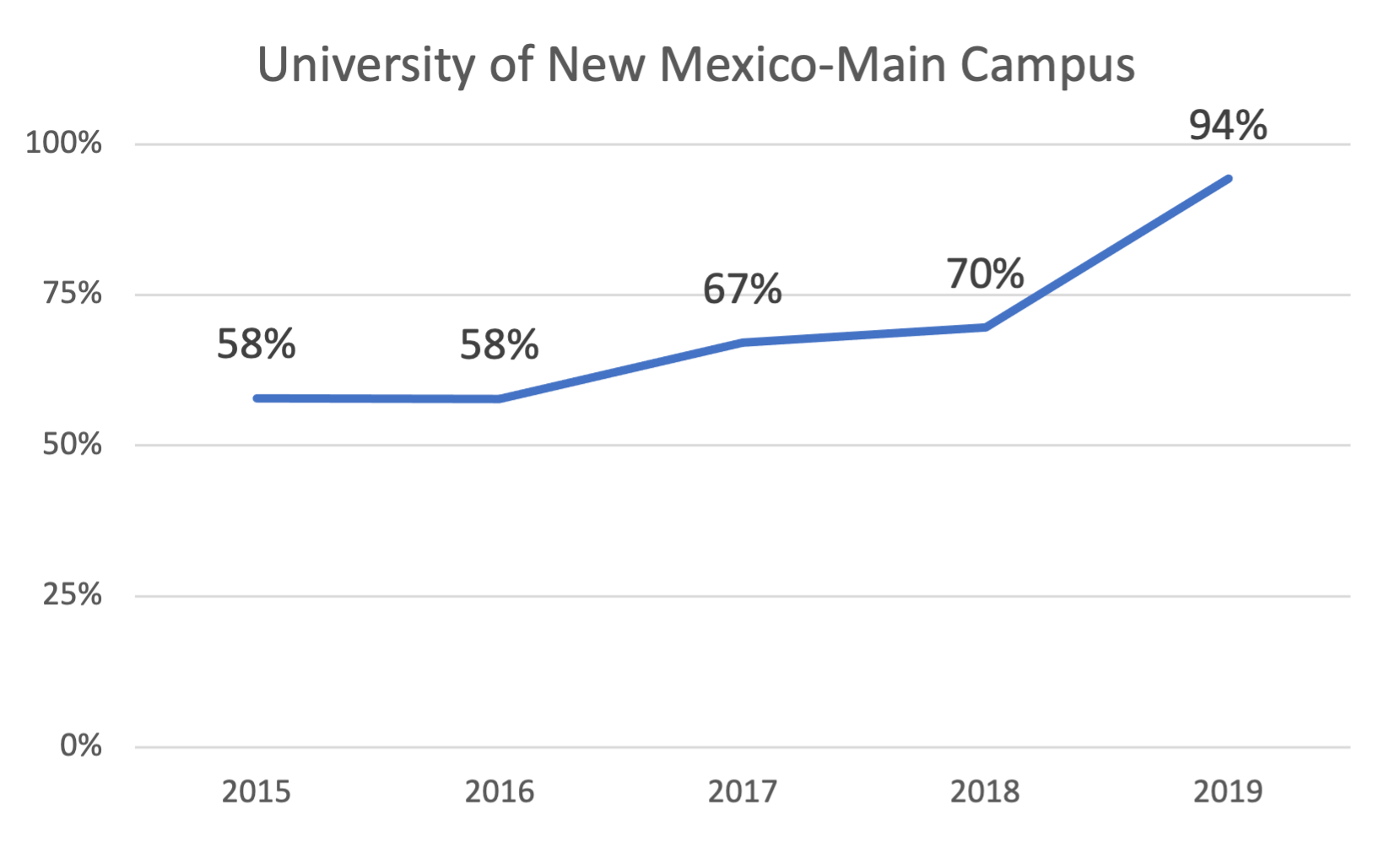

UNM has a small out-of-state contingent (14% in 2019) so this is almost entirely the result of in-state trends. The schools looked at in this post have generally had stable admissions rates, but the UNM has not done so well on this metric, going from light selectivity school to essentially open admissions by 2019.

Besides having difficulty attracting applications, accepted students were less and less inclined to enroll.

One can trace the impact of the UNM’s administration decision on the financial aid budget through the timeline: a) Cut the financial aid budget in 2018; b) Yields and enrolling class size subsequently decline that year; c) Increase the admissions rates in 2019 as a reaction leads to further declines in yield. With a mediocre 77% retention rate for returning 2nd years, and the fact that UNM is essentially admitting anyone who wants to attend, price cutting is logically the next step. UNM administrators fought pricing and the pricing won.

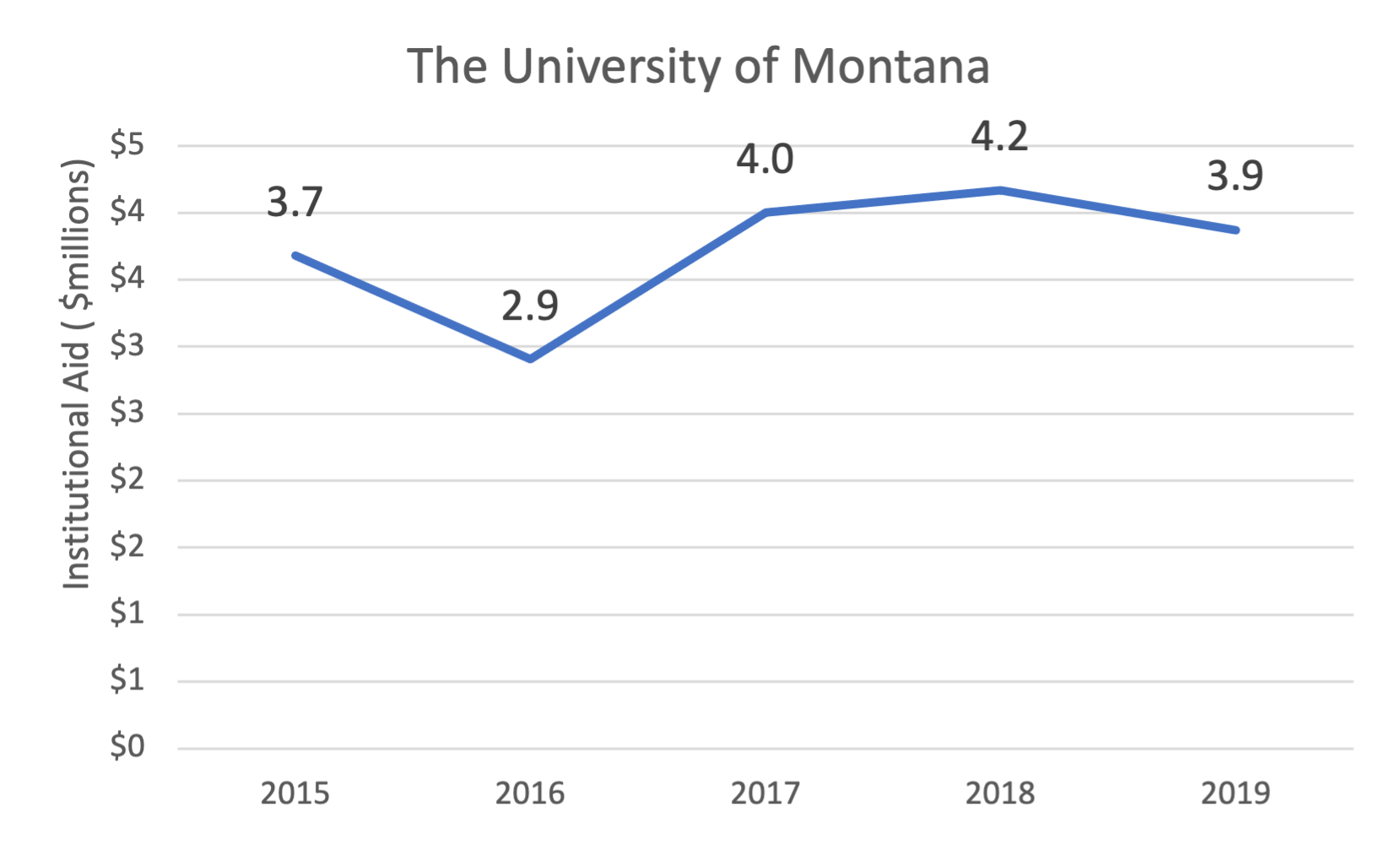

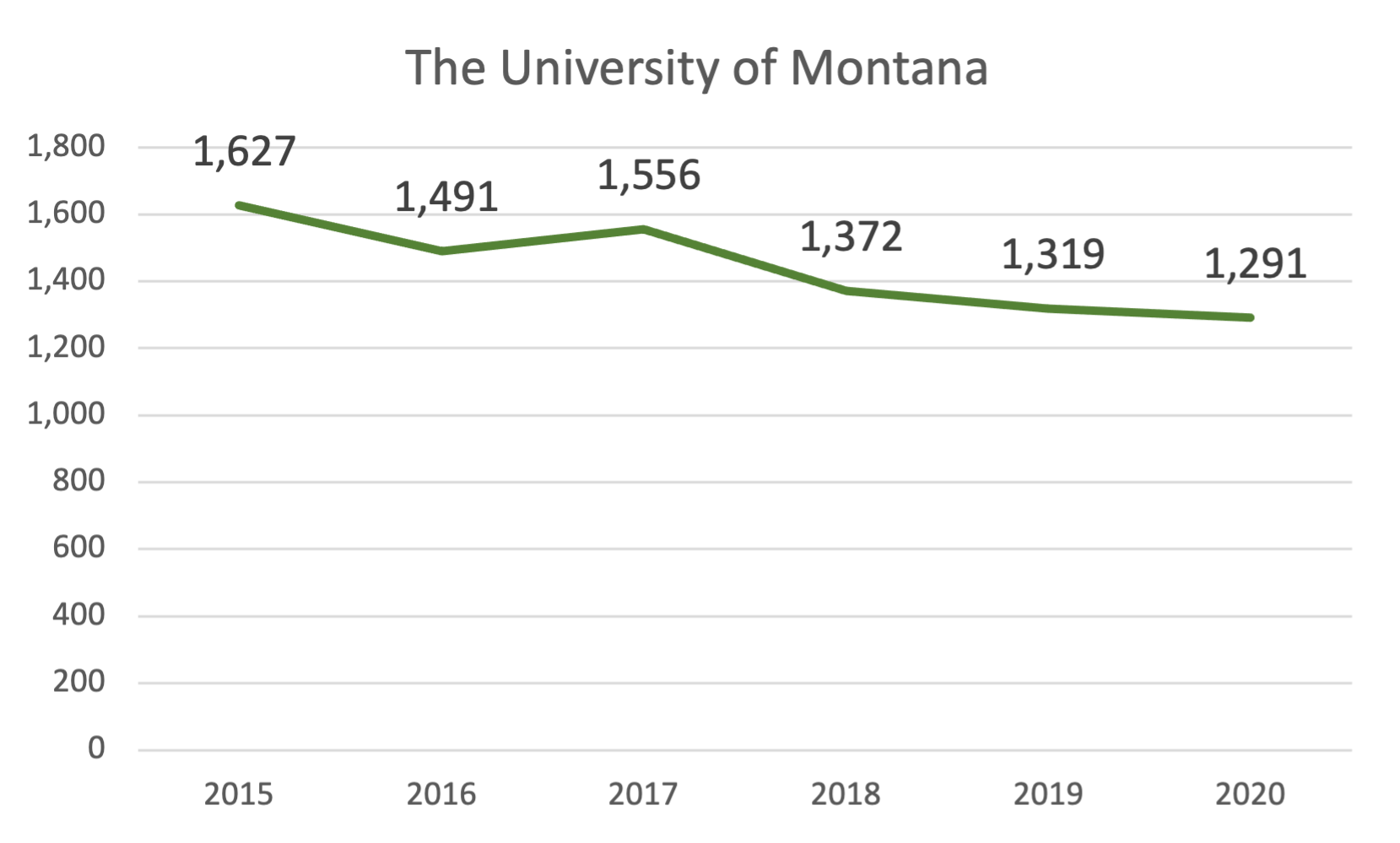

Farther north, the University of Montana in Missoula (the state's 2nd largest public university) also held the line and refused to increase its financial aid budget, at least on an absolute basis.

Holding the line had a clear impact on enrollment.

Montana admits nearly all applicants (94% in 2019), so it will likely need to lower its net prices and increase its financial aid budget to try and recover enrollment.

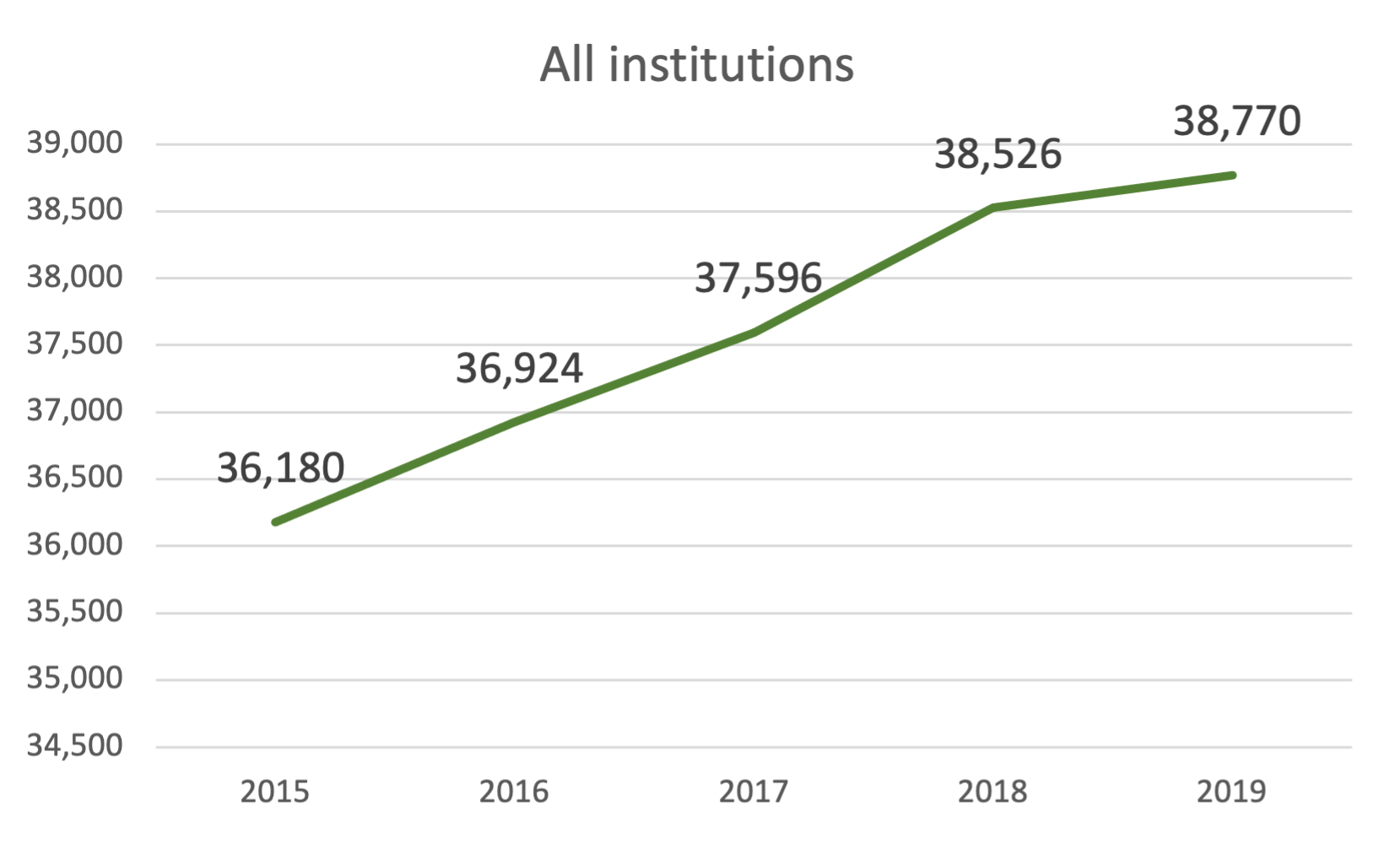

These enrollment losses occurred within a favorable environment of climbing first-year enrollment for comparable state schools. If we look at all the schools surveyed, entering classes increased nicely in size.

As we have remarked previously, undergraduate is today a business that is highly price sensitive. Montana and New Mexico bucked the regional trend, shunned discounting and lost students.

The results defy conventional causes

These results are striking because the drop in these colleges' market power is seen despite favorable drivers.

Price declines seen in the face of larger high school graduating classes? Check. This is one of the more interesting observations. Demographics are seen as a key driver behind potential higher ed revenue issues. Yet we have a public college sector operating in a very favorable demographic setting - with an inability to raise prices.

Price weakness in the face of a very good economic environment? Check.

Price weakness at "importer" publics with large numbers of out-of-state undergrads? Check.

Price weakness at publics with relatively little out-of-state recruitment? Check.

Attendance impact from schools tha held the line on their financial aid budgets? Check.

We will hold off on drawing conclusions or attributing causal effects until more schools have been studied. But a favorable economic and demographic situation didn’t spare these Rocky Mountain public colleges from adverse trends.

Next, we will look at the public school sector in the deep south. The University of Alabama's recruitment prowess may draw a lot of attention but several of its regional competitors are signaling enrollment distress.

Read this post and others at the CTAS site.