2024’s College Cost Reduction Act

It’s only a proposal currently but may influence federal changes to aid and loans

With the shake up in DC continuing, it’s worth looking at a congressional proposal made in January 2024, the College Cost Reduction Act (HR 6951). Any in-depth look at congressional proposals may be premature because so many die in committee or the floor, but this one looks increasingly relevant as it was resubmitted with a large group of largely Republican co-sponsors immediately following November’s presidential election. The lead actor is Virginia Foxx (R-NC), who worked as both a college instructor and then a community college administrator before moving into politics, and who served as the Chair of the House Committee on Education and Labor through 2024. The proposal is multifaceted but one important provision ends the Plus loan program, which includes the Parent Plus Loan program used for undergrad loans and the Direct Plus program used by grad students.

The proponents of the bill argue, plausibly, that the Plus programs help drive up college costs by allowing borrowing up to the college’s cost of attendance, a cost set by institutions and one which typically rises annually. The proposal eliminates the Plus programs and centralizes student loans in the Direct Student Loan program, currently capped at $31,000. The new rules raise the caps for total Direct Student Loan borrowing to $50,000 (undergraduates), $100,000 (graduate students) and $150,000 (professional degrees). This increase is for unsubsidized loans and, as far as I can tell, does not raise the limit on subsidized Direct loans.

Comments:

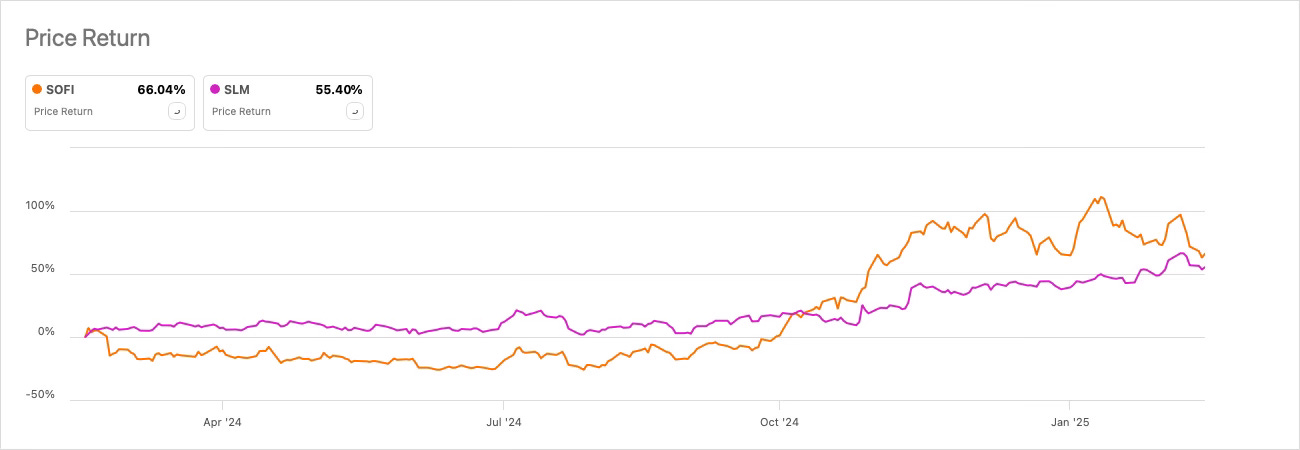

The stock prices of both SoFi and Sallie Mae (renamed as SLM Corp.) have rallied sharply in the wake of Trump’s election victory. These two companies are leaders in the private student loan market and, though it is always guesswork when trying to connect cause and effect in long-term stock movements. Investors may have bought up shares due to the increased chances of HR 6951’s initiatives being implemented. An elimination or reduction in the Plus loan program could increase opportunities for both companies as borrowers would lean more heavily on the private loan market, gutted in a 2010 Obama administration restructuring.

A 2024 study by the Education Data Initiative calculated that the average undergrad Direct Loan borrower owes $25,670 in federal Direct student loans and that the average Parent Plus loan borrower owes $30,500. While many students don’t go into debt to pay for college, a segment of undergrads use debt to afford some of the high net prices charged by certain colleges.

My personal opinion is that the $50,000 undergrad loan limit in HS 6951 is a lit fuse under the higher priced portions of the undergrad marketplace. It could force a lowering of prices and further staff and institutional consolidation. While some students will rely on the private loan market to make up for the capped loan limits, many others will either balk at the loans, which often charge higher interest, or fail to pass credit checks. This may dramatically affect students’ ability to pay, right in the midst of the misnamed Demographic Cliff (hint: it’s not a “cliff”, it’s a slow and gradual decline in the number of graduating high school seniors), for a double whammy.

An important detail to note is that these limits will also have a significant impact on medical schools. The average graduating medical student has a debt load of $191,950 associated with graduate studies (same link, scroll down a bit). The proposed limit of $150,000 will either force students to borrow from other, private sources or for medical schools to hand out more aid to reduce their net prices. (Professional degrees like JDs and MBAs have average borrowings below the $150k limit.)

While the Biden administration’s SAVE repayment plan is now dead as a doornail, HS 6951 solidifies the position of the less generous ICR (Income Contingent Repayment) plan by again codifying it. The current administration has also floated the idea of transferring the federal student debt portfolio to the Department of Treasury, headed by a long-time friend of Trump’s, Scott Bessent. Changes to federal repayment plans are in play and may be significant.

To me, this student loan program restructuring would likely have much larger consequences for the education industry than the more heavily publicized GOP proposal to increase taxes on the larger university endowments. Republican House representatives in January presented a bill that would raise the tax rate on selected university endowments from 1.4% to 21%, aligning the corporate rate with investment income generated by financial institutions and, in general terms, equalizing the tax status of for-profit and non-profit investment firms. These endowments are heavily concentrated in a few prestige schools, so any such tax would affect few universities and students. (For example, if you consider the top 10 endowments for California schools, Stanford’s is larger than those ranked 2-10 COMBINED.)

One other important idea circulating in congress is the idea of taxing aid awards. This would drastically change the way colleges price and award aid and would incentivize tuition resets. 2017’s Tax and Jobs Creation Act has several important rules terminating at the end of 2025, including the elevated standard deduction and higher estate tax exemption levels. That means that Congress will be deciding on whether to extend the TJCA provisions, which are popular, and it will likely need to find new revenue sources. Taxing aid awards would, according to an estimate in the linked Forbes article above, generate $54 billion in annual federal tax proceeds. I think such a number will never be generated but changing this rule would in one congressional action strongly encourage transparent college pricing, the reset of the cost of attendance to the real net price, and may force large structural reforms in today’s overcomplex system of merit and need-based aid.

Returning to HR 6951, some other changes it proposes:

The bill mandates that all student financial aid award letters must include both direct and indirect costs. This is a welcome reform.

It eliminates federal student loan origination fees. These fees are not large for the Direct Student Loan program (they are onerous for the Parent Plus program) but again this represents a welcome development.

Significantly, Section 492A of HR 6951 sharply restricts the ability of the Secretary of Education to increase federal costs associated with higher ed, a change related to the Supreme Court’s overhaul of the Chevron doctrine (June 2024). With the Department of Education potentially being dismembered, it’s unclear how important this part of the proposal is. (A related proposal establishes a form and process for new terms being imposed on loan servicers.) I suspect these rules are in reaction to what are viewed as abusive actions by the Dept. of Ed under Miguel Cardona.

Sec. 323 at the very end of HR 6951 proposes what looks like a technical reform to the transfer of credits between institutions. If a reader has insight as to the significance of this particular proposal, please leave a comment or send me an email. I will be happy to add the comment right here in this post.

Though it may be premature to cover proposed legislation, given how often proposals die in committee or on the floor, this initiative is important enough to think about due to the strength of support it received in the House. And investors in SoFi and SLN may agree.

This material is intended for educational purposes only. You should always consult a financial, tax, or legal professional familiar with your unique circumstances before making any financial decisions. Nothing in this material constitutes a solicitation for the sale or purchase of any securities. Any mentioned rates of return are historical or hypothetical in nature and are not a guarantee of future returns. Past performance does not guarantee future performance. Future returns may be lower or higher. Investments involve risk. Investment values will fluctuate with market conditions, and security positions, when sold, may be worth less or more than their original cost. Avise Financial Cooperative, Inc. is a registered investment adviser with the SEC. Registration of an investment adviser does not imply a certain level of skill or training.