Retention: Private colleges in the Great Plains

NGMI? Ground zero of a looming cluster of college closings?

How do we know whether a college is running an effective undergraduate program? Retention – the % of first-year students returning for a second – offers an up-to-date metric. While it isn’t the be-all-and-end-all - other measures and information are important in “grading a program” - retention offers a bottom-line result measuring whether students can do the course work, can afford to pay for the program and, finally, like what they are getting from the college. Because retention at different classes of institutions isn’t comparable, this series tries to decompose what retention is telling us about schools in a given category and region to allow for valid lessons.

The Great Plains states host scores of small private colleges alongside their networks of public universities and community college systems. The numbers are remarkable: 20 private colleges currently operate in Iowa, a state with a population of just over 3 million. Missouri is home to 27 private schools with enrollments over 1,000 students. Neighboring states have similar concentrations. To put this in context, if California had the same number of private colleges per capita as Iowa, it would have 245 (it in fact has about 50 of size). The host includes some very well-known and successful ones – such as Wash U in St. Louis and Grinnell – but many have a questionable future.

So far, these institutions have hung on. There are few reports of imminent closures. Which ones are doing well and which are not? The retention stats do in fact present a clear division between colleges performing in line with national expectations and a second group where student satisfaction points to problems. Prior posts in this retention series have generally shown a cluster of results with a few outliers on the positive or negative side. The results for the Great Plains don’t look like this at all. They are “bimodal” with two clusters: one includes some well-known and successful schools – Carleton and St. Louis University would be two other examples – but a second seems to exist in a completely different sphere – a much inferior one – of student success.

NGMI? (Not gonna make it?)

Let’s deal with the bad first. This post will look at struggling colleges and a follow-up will move on to the region’s more successful programs, those with results more typical of the rest of the country.

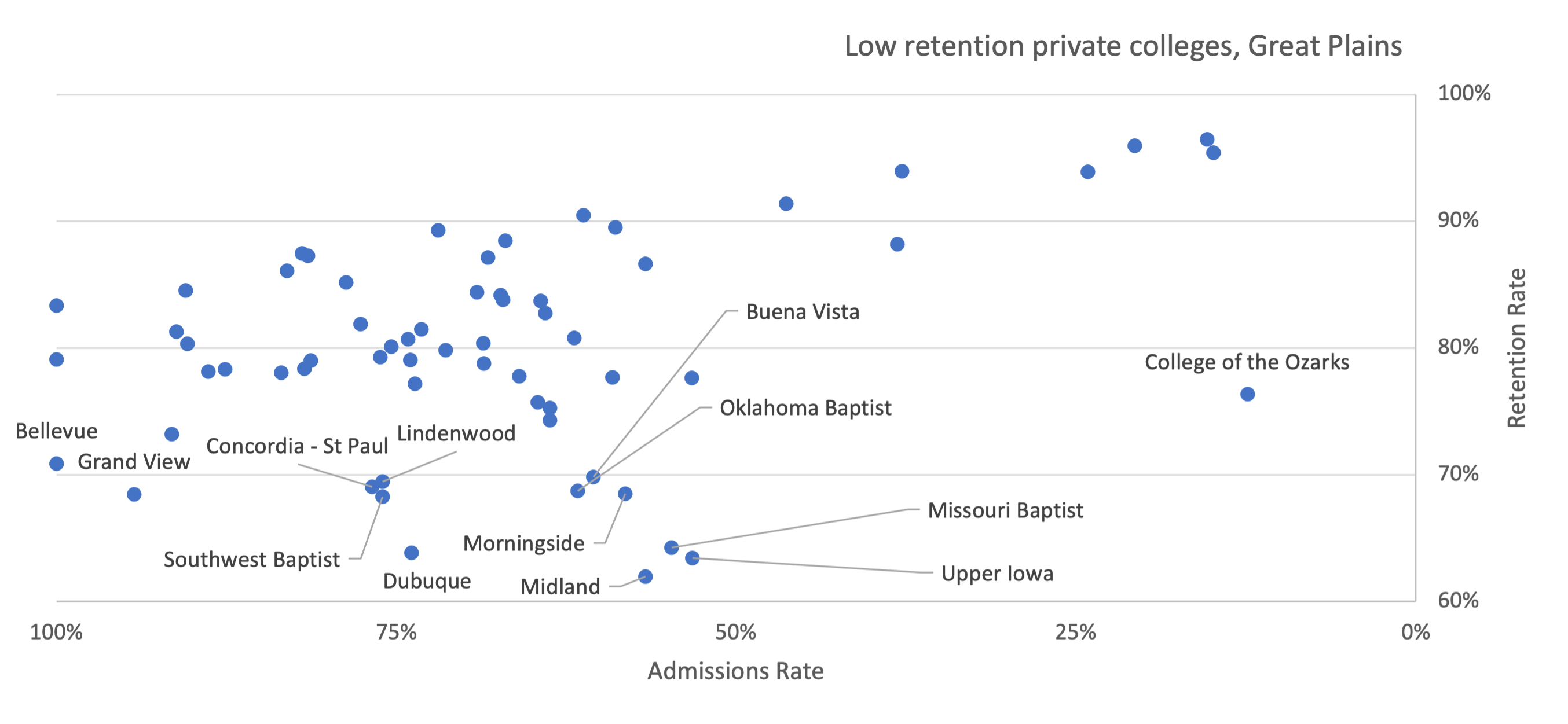

A broad graphic displays the region’s bifurcation:

Readers of the e-mail can click on charts to see them magnified.

The first group of schools – the “Normal” — display standard levels of retention as compared to admissions rate. Some are better than others but, even for those that are below average, the numbers aren’t unusual. What is striking – and not seen elsewhere in the US – is a smaller group - the “Troubled” — with results falling well below the normal zone.

The University of Dubuque in Iowa on the Wisconsin border is one of the “Troubled”. It loses over a third of its entering class each year. That’s an average; some years are worse. In 2017, 41% of the prior entering class left within a year. The university also experiences large fluctuations in recruiting success, enrolling a high of 516 new full-time undergrads in 2018 but only 384 the next year. Dubuque is not in crisis – its student body size has grown a bit in recent years – but the economics of running a program where a third of the entering class leaves before the next academic year makes the whole affair a juggling act.

Dubuque is representative. Many colleges retain under 70% of entering students with several more producing very mediocre results just above that level:

Located anywhere from Oklahoma to the Twin Cities, these are colleges which are not in crisis, per se, but whose retention results point to students unprepared for the school work or dissatisfied with what they find.

Midland University, outside of Omaha, Nebraska, serves as another example. It is actually fairly selective, accepting only about half of applicants. But Midland’s retention stats are positively dismal for such a level of selectivity: reliably, year after year, 4 out of 10 entering students leave by their second year. The disconnect between the retention and admit rates raises the possibility that the admissions office is aggressively managing its selectivity metric by rejecting academically strong applicants with the view that they wouldn’t actually enroll there.

While we have previously avoided providing tables and lists to make this retention series more readable, we’ll make an exception here to help inform students about which colleges are in the “Troubled” set:

Results like this makes it difficult for colleges to function. As a reference point, when Concordia in Portland closed, it was stumbling along with a retention rate of 50%, the sign of a very troubled school. College closings are of course only partly caused by enrollment issues. A sizable endowment can dampen recruiting pressures. Among those listed above, Lindenwood has the most substantial endowment. Standing at approximately $200 million, it is about ten times the size of Midland’s small fund, giving it more cushion to survive shortfalls than the others and much better survival odds. On a per student level, these schools’ endowments on the whole are no match for some of the nation’s richer institutions, though. This means that they all depend on tuition revenue from a stable student body and that, while they don’t approach Concordia-Portland’s final level, their retention makes the risk of a descent into crisis real.

Why don’t these schools merge?

In the for-profit sector, a fragmented and troubled business area like this would be rolled up. One of the colleges with an ambitious administration would band with an investment fund and start acquiring the others, combine operations, expand marketing presence and re-establish the whole enterprise on a sound footing. Imagine if the schools in the chart above joined together. With a combined count of about 30,000 undergrads, a variety of grad programs on offer, and the ability to really brand and recruit, a regional powerhouse would be born.

But no such roll-up is happening. We can only speculate why, but the scarcity of mergers in the higher ed perhaps points to fundamental flaws in non-profit corporate organization and in the incentives for the administrators of these institutions, motivating for stasis and inertia even in precarious situations. Add to that how traditional education is tied to a location with staff and, in the case of these Great Plains institutions, mostly unsaleable physical facilities rooted in far-flung towns. And some of those on the list are denominational and perhaps incompatible in terms of philosophy. All these reasons may discourage the sort of business rationalization which is routine in the for-profit sector. But if this tendency to inertia is to be broken, the Great Plains may be the best candidate in US higher ed for a new approach.

Fortunately, the majority of private institutions in the central plains deliver solid results that are closer to the nation’s as a whole. Our next installment will look at these.

Find more information at the CTAS site. CTAS provides data, reports and personalized assistance with college pricing and aid appeals.