Takeaways from our series on Southern Higher Ed

Takeaways from our series on Southern Higher Ed

Pre-COVID Higher Ed: Southern public universities

Over several posts in the last few months, we have looked at the evolving commercial situation of public universities in the central part of the south (Alabama, Mississippi, Tennessee, Louisiana and Arkansas) in the years leading up to COVID. Several of these schools received a more extended review, including the University of Alabama, Mississippi State, LSU and Southern Mississippi.

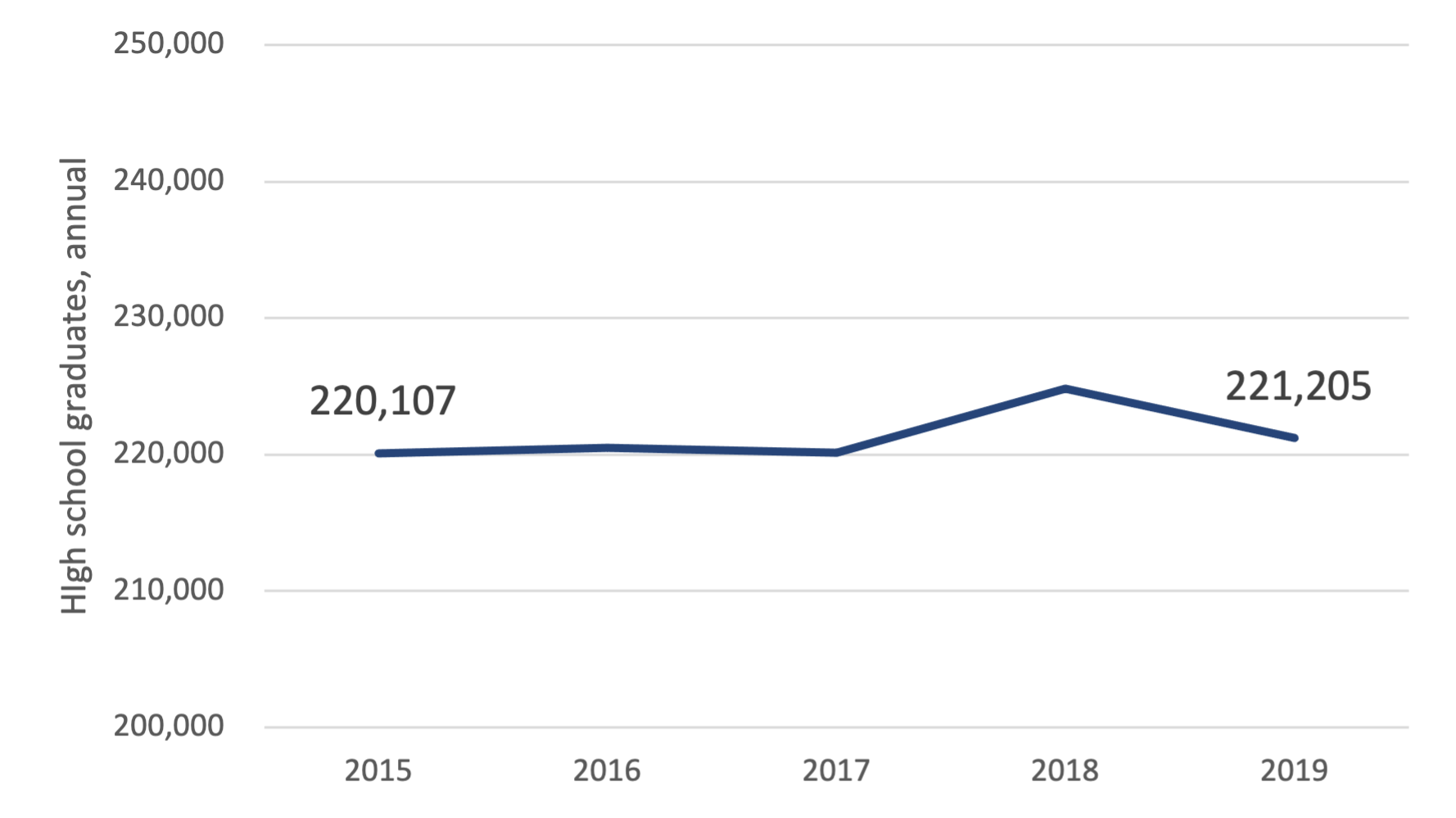

The states in our spotlight showed demographic trends similar to what the US as a whole will encounter in the 2020s, with flat high school graduating classes:

In response, the schools regularly displayed energetic and resourceful reactions. Even their mistakes (e.g. the University of Alabama’s 2018 net cost hike) are instructive because what these universities encountered anticipates the situation across much of the US in the next decade:

Student price/enrollment behavior suggests that many undergraduate degrees are close to being perceived as a commodity (an undifferentiated product or service).

Consumers become very cost conscious when paying for a commodity. Institutions can look like they have significant market power when in fact they don’t. The University of Alabama’s 2018 price hike mentioned above provides one example: Bama raised its prices and immediately encountered obstacles and sagging enrollment despite years of tremendous recruiting success.

Can marketing offset commodification? It looks like it can sometimes. One of the most impressive marketing overhauls we looked at - LSU’s in 2018 - achieved its results by combining improved marketing with lowered pricing and a larger financial aid budget, so the example doesn’t provide unambiguous support for marketing as a solution. The University of Memphis was able to generate what looks like a permanently higher application level, presumably with the help of improved marketing and outreach, but the shift included a changed application process, so it too was not a pure example of marketing.

Market-sensitive enrollment strategies pursued by private colleges are seeping into the public sector as high school class sizes flatten out and the publics work to poach out-of-state students. Examples:

Alabama’s humongous financial aid budget, adjusted with sensitivity to the market reactions in an enrollment cycle, generates large discounting almost in line with NACUBO surveys of private schools.

The attention to marketing and recruitment process shown by schools like LSU and the University of Memphis.

Execution of a tuition reset by Southern Mississippi to more accurately convey to prospects the university’s net cost.

“Prices or enrollment or admissions standards – pick 2”

None of the publics we looked at were able to simultaneously raise prices, tighten admissions standards and maintain enrollment.

Mississippi State saw this play out: it maintained enrollment and admissions standards by keeping pricing flat.

The University of Arkansas experienced a variation: it maintained enrollment and raised prices by loosening admissions standards.

Institutions regularly flash an “unwind” pattern involving admissions %, yields, pricing and financial aid budgets.

Throughout our survey of these Southern publics along with an earlier exploration of the equivalent universities in the Rocky Mountains, we repeatedly saw a sequence of events where a school raised (or tried to raise) prices and then had to react by lowering admissions standards to maintain enrollment, thereby approaching open-enrollment status. The next step in the sequence consists of increases - often steep ones - in the financial aid budget, with flattening net costs, and declines in yield. The experience of the University of New Mexico provides one typical story.

Southern Mississippi represents an unusual example because it sacrificed admissions standards and yield while lowering - not increasing — its financial aid budget. This was an out-of-consensus action that stands out from common patterns.

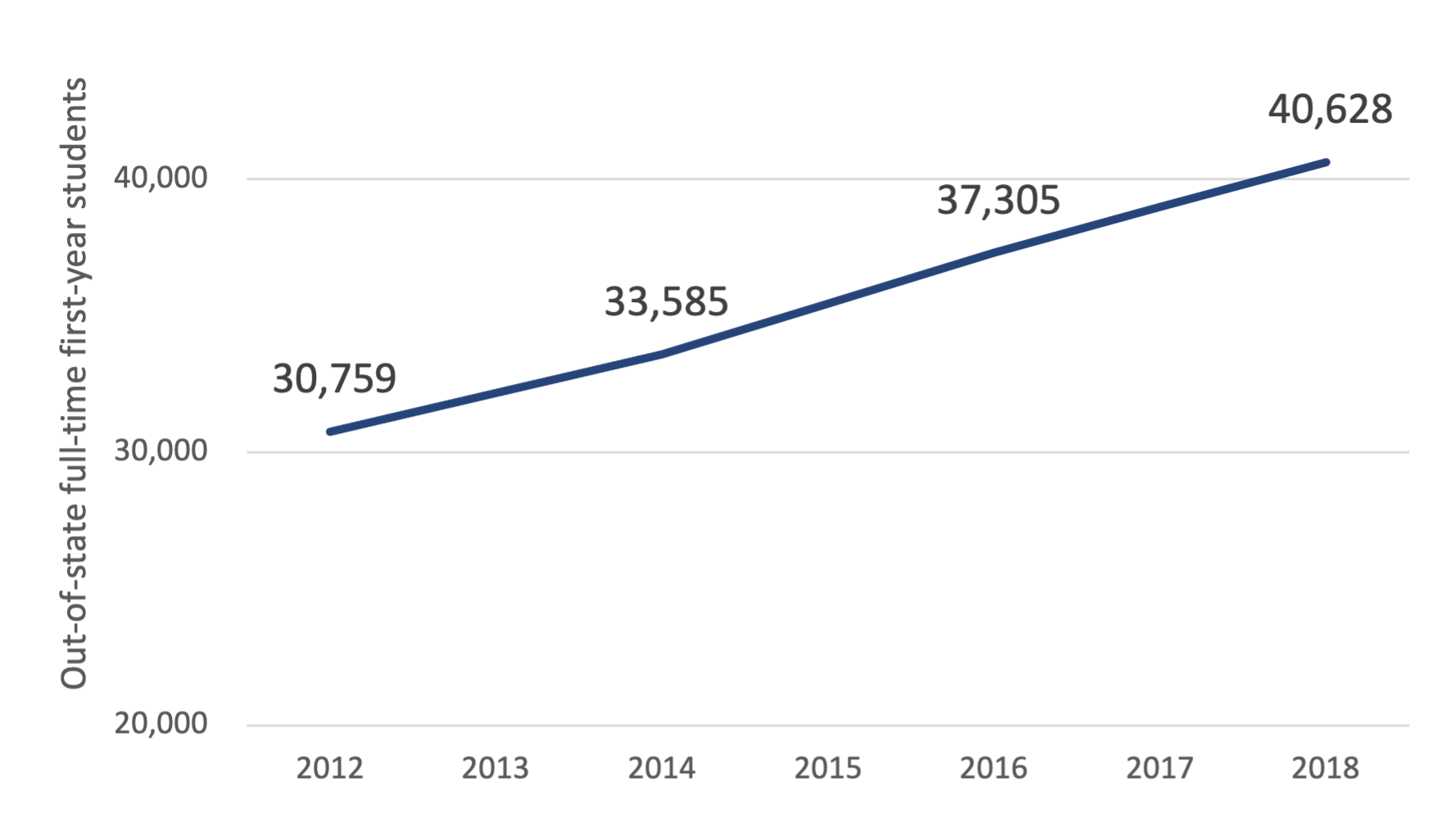

Schools in the Southern region we covered - both in our subset of large public universities and in all private and public colleges - did succeed in increasing out-of-state enrollment (see chart below) but the market is competitive, tight and risky.

Only the paranoid survive: the University of Mississippi had conducted a disciplined and successful out-of-state recruitment effort nearly the size of Alabama’s before encountering a setback, which by the looks of it took their management team by surprise. In fact, Mississippi hadn’t been doing anything wrong. But other schools, including LSU, suddenly ramped up their efforts and Mississippi out of nowhere lost first-year students and had to pare back its operating budget.

Several smaller colleges beyond the large publics in our focus set succeeded in making step change gains in their out-of-state recruiting, including Tennessee State (in Nashville), Jackson State in Mississippi and University of Alabama-Huntsville as well as private schools like Tulane and Xavier in Louisiana. All of these colleges are eager to snap up students the moment a larger public university looks for whatever reason less attractive.

We won’t presume to provide guidance on how colleges should behave in this situation, but there are possible lessons:

Commodified markets do see instances of marketing successes, but these successes swim against the tide and can evaporate quickly.

What approach works in a commoditized market? Cost control, cost control, cost control.

Commodity market pricing goes up when demand exceeds supply. US higher ed is saturated with oversupply. It’s unlikely this changes in the foreseeable future.

These last two points segue into an account of US inflation in higher education and at the general economy-wide level, upcoming here later this month.

Read this post and others at the CTAS site.