Why CTAS uses family income, not the EFC

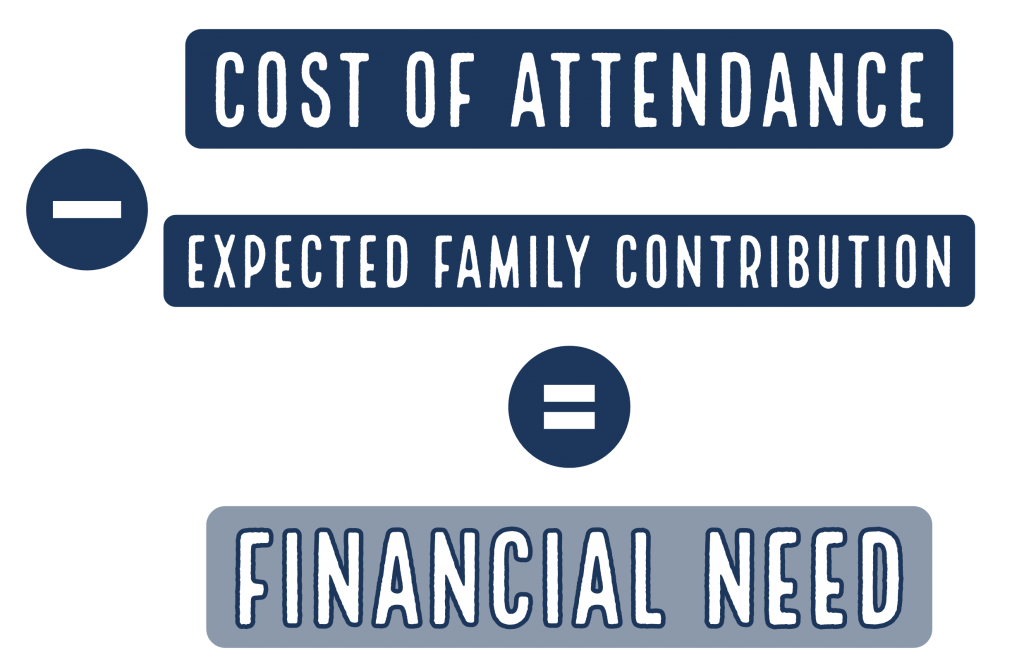

Why CTAS uses family income, not the EFC

Students aren’t “price takers"

We were asked on Twitter recently whether it wouldn’t be better for CTAS to chart prices according to the Expected Family Contribution (EFC, soon to be the Student Aid Index), rather than annual family income. The answer is “no”.

The EFC is a federal statutory financial aid formula, not a market price. College enrollment is a market.

The EFC includes assets as a resource to pay for college. Parents are refusing to price based on assets. (And we’ll argue that colleges shouldn’t want to, either.)

No one knows what their EFC is. It’s not used for financial planning.

When the Dept. of Education’s National Center of Educational Statistics implemented the net price metric, it used family income to segment the pricing data, not the EFC, implicitly supporting our position.

EFCs are more unpredictable than incomes.

College aid offers ask students and parents to provide more funding than the EFC dictates much of the time. So why even refer to it at all?

Let’s look at some of these reasons in more detail.

What is your EFC?

Parents don’t know what their EFC is. (Quick: what is yours?) It is both conceptually confusing and requires work to determine. (Inputting data into an EFC calculator makes watching paint dry look like entertainment.) And schools tweak the federal formula to arrive at their version of need anyway, so there’s ambiguity even after you’ve done the work.

CTAS relies on family income to provide a familiar reference and help simplify a confusing price environment. Sharing our objectives, the Department of Education intended to provide transparent and clear information to students and families when it created the Net Price metric and tied the reporting buckets to annual family income. CTAS has the same goal and presents data along the same axis, without the destructive interference inflicted during the implementation of Net Price, which we are guessing came from lobbying by universities.

The EFC Asset Conversion Ratio is unsustainably high

The EFC is of course generated by household data, income and asset inputs, using a progressive formula with exclusions and allowances at certain thresholds. Colleges price using the EFC, at least formally, asking families to use their assets to pay for college. The EFC formula assumes that up to 5.7% of parental assets will be used after an exclusion, a number after taxes. That percentage dictates that, for a number of years, families turn over the entire returns from their investment portfolio to fund college -- and then some.

What’s the basis for this 5.7%, anyway? It seems like analysts in the Department of Education looked at some investment returns a couple of decades ago, for reasons unknown applied a 12% rate (?) to families’ asset base and then looked at this number, thought this way too high, and multiplied this 12% by 47% (??). What’s the logic here?

Today, with the 10-year Treasury note sitting at a yield of 1.75%, before taxes, there is a complete disconnect between the EFC asset conversion formula and plausible market returns on an investment portfolio. Both the origin and level of the number are suspect. Using it is unwise on a number of levels. There’s absolutely no reason for a reasonable parent to look at this formula and think it is a sound basis for price-setting.

A contested environment

Given that college is such a major life expense, the use of an abstruse, unusual formula to determine prices customized for individual students is bound to create resistance. Especially because the EFC so often exceeds what families budget for college or feel they can afford. But college administrations have traditionally thought in terms of EFC and would like to use it. This makes use of the EFC contested territory.

When one side of a transaction has complete market power, that side can indeed impose the pricing mechanism and level it wants. And there is a portion of higher ed that has that kind of market power: the highly selective Ivy+ schools, with their very low admissions rates. What do those Ivy+ colleges do? They price based on need, with low-levels of non-EFC based institutional aid. We don’t know exactly how these need formulas work, but they have principles in common with the EFC and include assets in the equation. And students accept it - because they have to.

But the remainder of higher ed programs, where almost all students enroll, don’t have anywhere near that level of bargaining power. In this group, use of non-EFC aid is heavy and growing as students leverage their awareness and tools to make colleges economically compete for them. Students here aren’t “price takers.”

The community college and national online segments price in ways that are different from either of the approaches contrasted above, so comments here apply to 4-year traditional schools.

Much aid doesn’t rely on the EFC

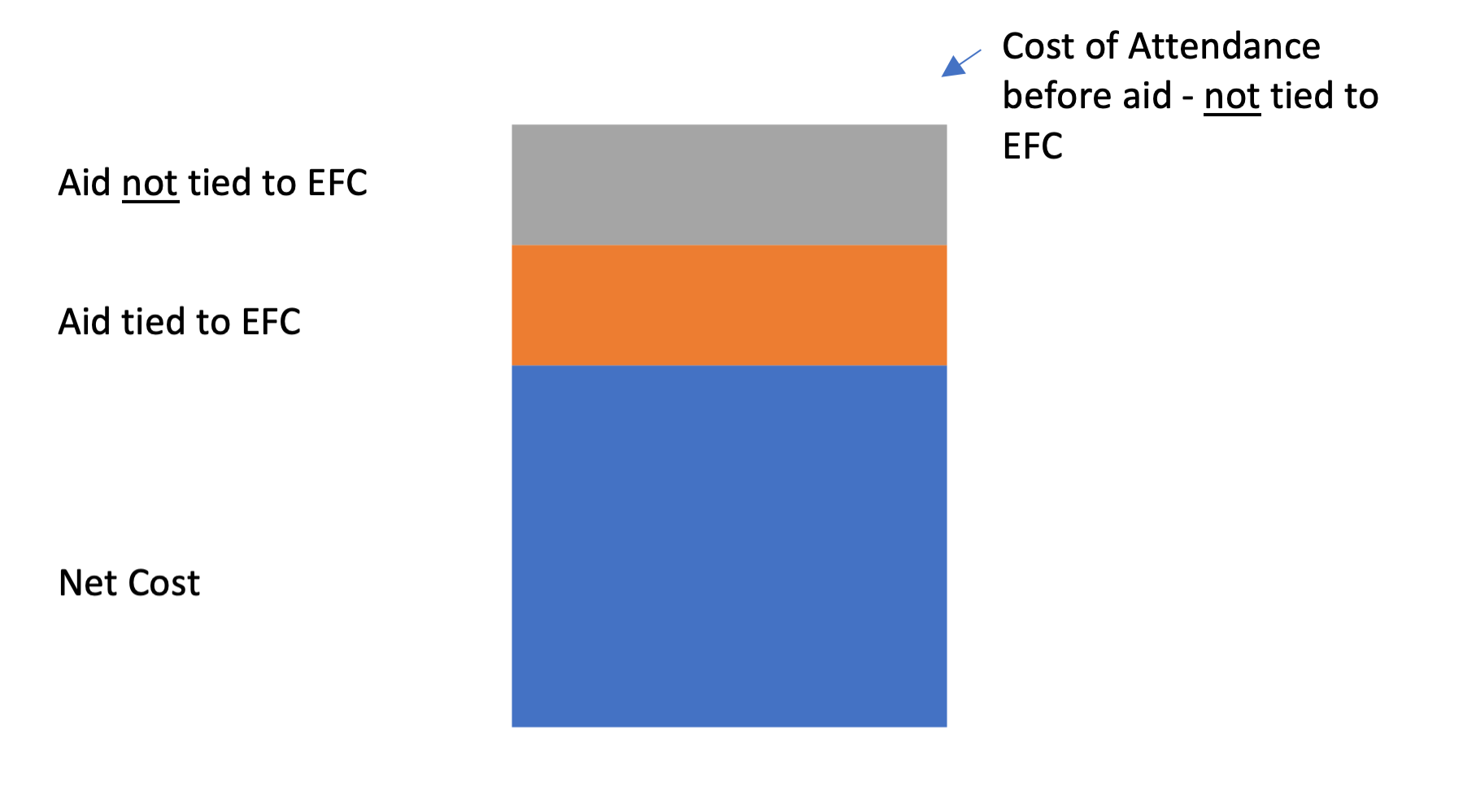

Another way to think about the topic is that non-repayable “aid” - discounts on the top-line cost of attendance — can be divided into two types, the aid relying on the EFC formula and the aid that doesn’t. Aid that relies on the EFC framework includes the Pell program, FSEOG, certain state formulas and, most importantly, the college’s own need-based calculations. Types that don’t rely on the EFC include merit aid, independent scholarships and certain major state education funding initiatives, such as Georgia’s (the Hope & Zell Miller programs) and Florida’s (Bright Futures). Because this last class of aid is significant, we can expect a large divergence between net prices and EFC on that basis alone. In fact, the numbers indicate that the two categories of aid are likely comparable in size.

Aid for first-years only at CTAS’s consideration set of 4,100 2- and 4-year colleges. The Pell Grant total is smaller than expected because certain educational institutions and students past the first year are excluded from this tally.

Institutional aid combines merit and need, in a proportion that likely can’t be determined, while certain state and local grants rely on the EFC. So we can’t use this data to arrive at precise quantities - but the rough proportions serve our purposes. We can conclude that aid that is unconnected to the EFC is a significant portion of the overall amount.

And changes to the topline Cost of Attendance are also separate from changes to the EFC so, over time, we would expect those two metrics to diverge.

This results in a situation illustrated by this graphic:

If the Net Cost is what is left after two types of aid have been subtracted from a topline Cost of Attendance, and the topline Cost of Attendance and part of. the aid are not tied to the EFC, then the Net Cost is not tied to it either. This chart illustrates the issue. Actual proportions are imprecise.

Asset values have diverged from college costs

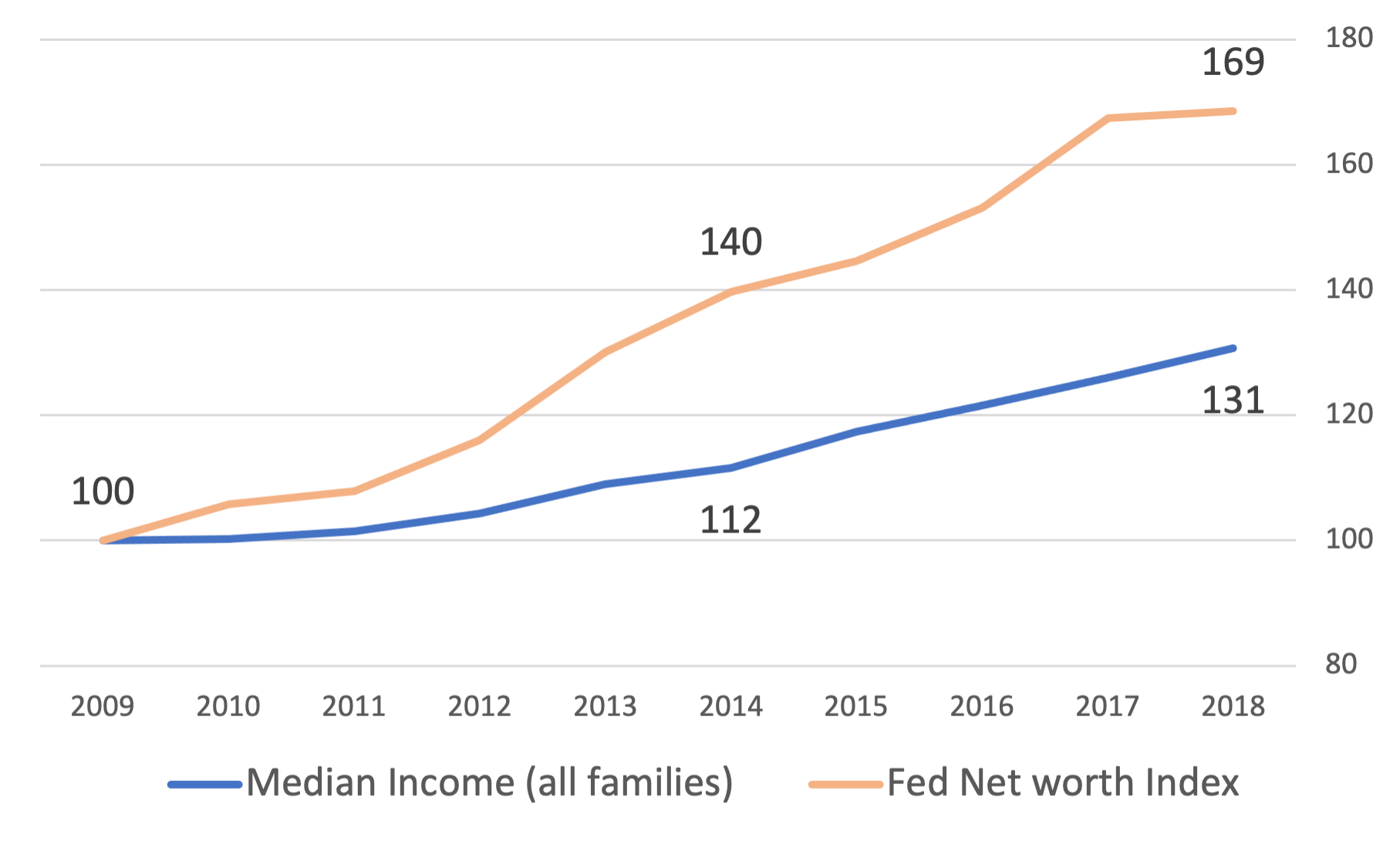

So the heavy use of aid not tied to the EFC suggests that family asset holdings or net worth will diverge from actual pricing. Does the data show this? One way of looking at this is through household asset holdings in the last decade. Measuring the assets - the wealth - of US families is complicated, with many metrics available, but all of them point to a complete disconnect between college costs, as measured correctly by Average Net Cost, and household wealth.

The Federal Reserve’s Net worth of Households and Nonprofit Organizations is one widely-used index. These are slightly outdated figures but they make the point well: college net prices and US net worth have diverged significantly in the last decade:

Other indices make the same point. Stocks? The S&P 500 was up 158% in the period above (vs 19% for college prices).

Residential real estate (used by some institutions in determining need)? Many indices out there but a widely-used one like the Case-Shiller 20-city composite shows home prices up 45% in the period above. Also very different from college inflation.

In practice - on average and with certain exceptions - asset prices haven’t had a significant impact on college pricing recently. Families have rejected the idea of basing college pricing on assets, investments and home values.

Asset values are more variable than income

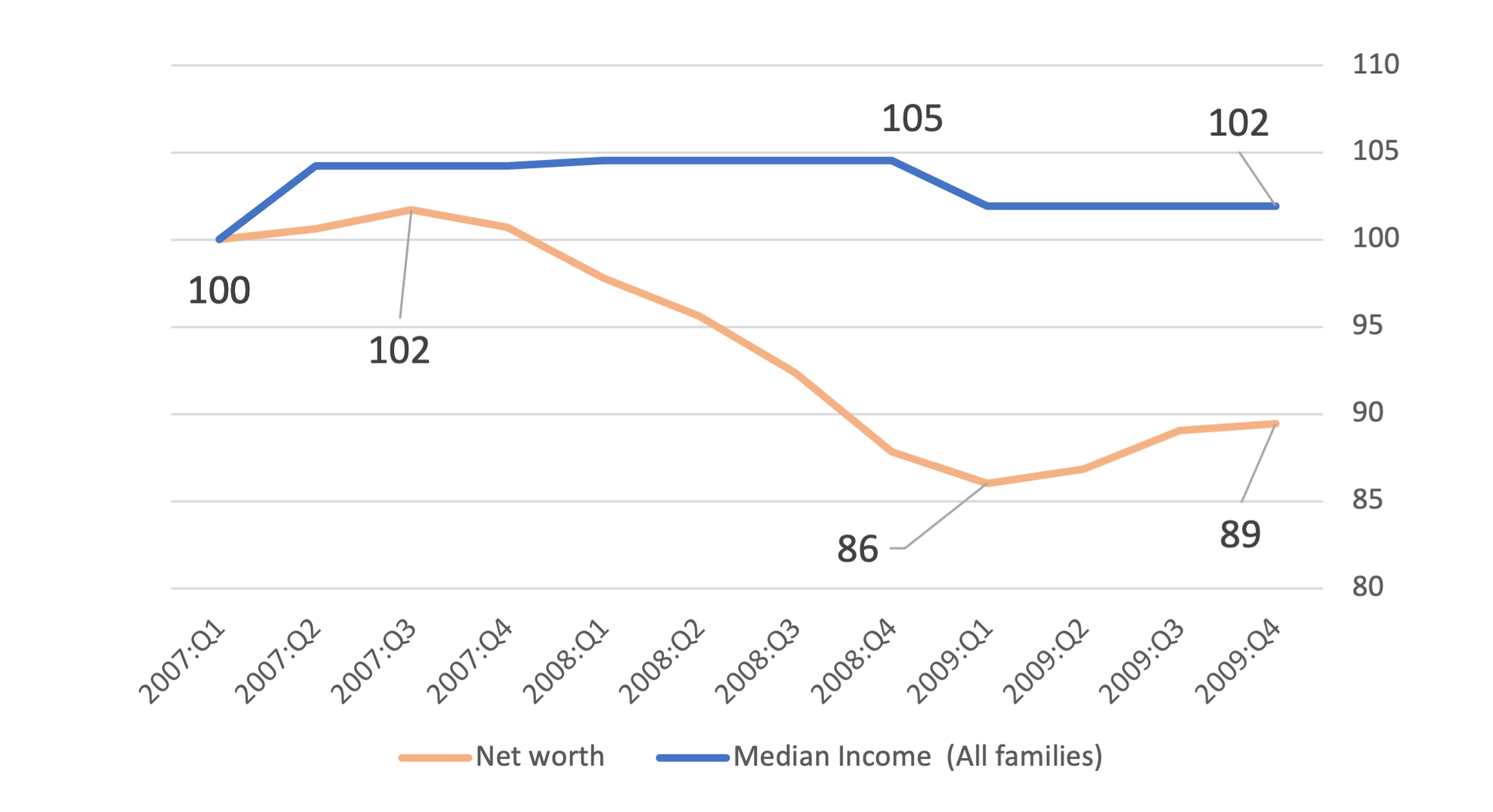

All of us have witnessed the volatility of financial markets as well as steep ascents and descents in real estate prices. In contrast, family income is relatively stable.

The 2009-2018 period would have permitted for faster tuition increases if assets were factored in pricing. But volatility works both ways. Below, see the Net worth index over the course of 36 months during the Great Recession, compared with Median Family Income.

Would colleges & universities have gone along with the portion of their tuition revenue dependent on family assets being slashed by ~15% over the course of about a year and a half? In a period when their endowments fell in value? Ivy+ institutions with their massive endowments can weather such shortfalls but less rich colleges simply cannot.

Colleges seem to be attached to the EFC formula - but the ones without large endowments, which is most of them, shouldn’t be. The volatility of assets makes them risky and unsuitable for price-setting for a service like education, with its high fixed costs.

Neoliberalism

To step back from the situation, higher ed is transitioning from a past state where collegial entities cooperated to educate students under a broad and highly regulated government mandate, into a new neoliberal environment emphasizing individual competing entities, voucherized government funding and market-based solutions. To quote Steven Mintz’s recent column “The Revolution in Higher Education Is Already Underway” from Inside Higher Ed:

The rise of the neoliberal university: The tendency of universities to act like private sector corporations, which is evident in shifting patterns of institutional governance, the adoption of enrollment management and other practices designed to maximize revenue generation, the relentless pursuit of ancillary income, the growing emphasis on return on investment, and the perception of students as customers.

The declining influence of the EFC is a financial manifestation of this rise.

TL;DR

Forgive the long-winded answer to why CTAS stratifies college costs by income. The short answer: it’s clearer for students & families and, because much of today’s higher ed enrollment operates in a marketplace more than a government pricing framework, family income is more relevant than a once-dominant but fading statutory mechanism like the EFC.

You can also read this post and others at our CTAS website.